When weighing up renting vs buying Australia, the old rules of the "Great Australian Dream" have changed. With current property prices, low vacancy rates, and steady interest rates, deciding whether to get a mortgage or rent and invest may be the biggest financial choice you will make in 2026. Choosing an investment strategy is ideal when it fits your actual life, so keep that in mind when exploring investment or home ownership options.

The "Great Australian Dream" in 2026

For a long time, the path to wealth in Australia followed a set pattern. You bought a house, paid it off, and retired. But in 2026, reaching that goal may require a different strategy.

Right now, the rental market is very competitive. Vacancy rates are at historic lows. Because of this, families are spending a record share of their income on household expenses.

There is a lot of talk about whether renting is "dead money." But we also have to look at the cost of a mortgage. With interest rates around 5.66% (as of March 2026 for Principal and interest according to Money Smart), paying the bank $50,000 a year in interest is also a major commitment.

As Financial Advisers at Peak Wealth Management, we look at these numbers as part of a bigger plan. Good financial advice is about more than just the balance on a spreadsheet. It is about funding the specific life you want to live. We help our clients look at the long-term projections so they can choose the path that gives them the most certainty.

Where Are You in Your Wealth Journey?

The right path for you depends on where you are starting from. Most people read this guide because they are at a turning point in their life. You might be in one of these situations:

- Looking to buy your first home: You want to stop renting and start building your own future.

- Already owning a home but wanting more: You want to grow your wealth by buying a second or third property.

- Thinking about "Rentvesting": You want to rent in the city where you work, but buy an investment home somewhere else.

- Looking interstate: You are looking for better growth or different prices in another state.

- Buying for investment only: You want to own property to build wealth, but you do not need it to be your actual home.

As financial advisers, we look at the parts of your life that most people miss. We look at your career path, your tax setup, and what your family will need in the future. These details make this a personal choice.

But one thing is clear. Building your wealth is the only way to find long-term stability. Owning property is a proven way to get there. Whether you buy now or rent and invest, the goal is the same. We want to help you find the best path for your specific life goals.

The 2026 Market: How the Rules Work Now

Making a smart choice starts with understanding the current property market. Right now, there is a low supply of homes for sale. This low supply keeps prices firm, even with current interest rates.

The property market also changes depending on where you live. Interestingly, in hundreds of Australian suburbs, it is now actually cheaper to pay a mortgage than to pay rent.

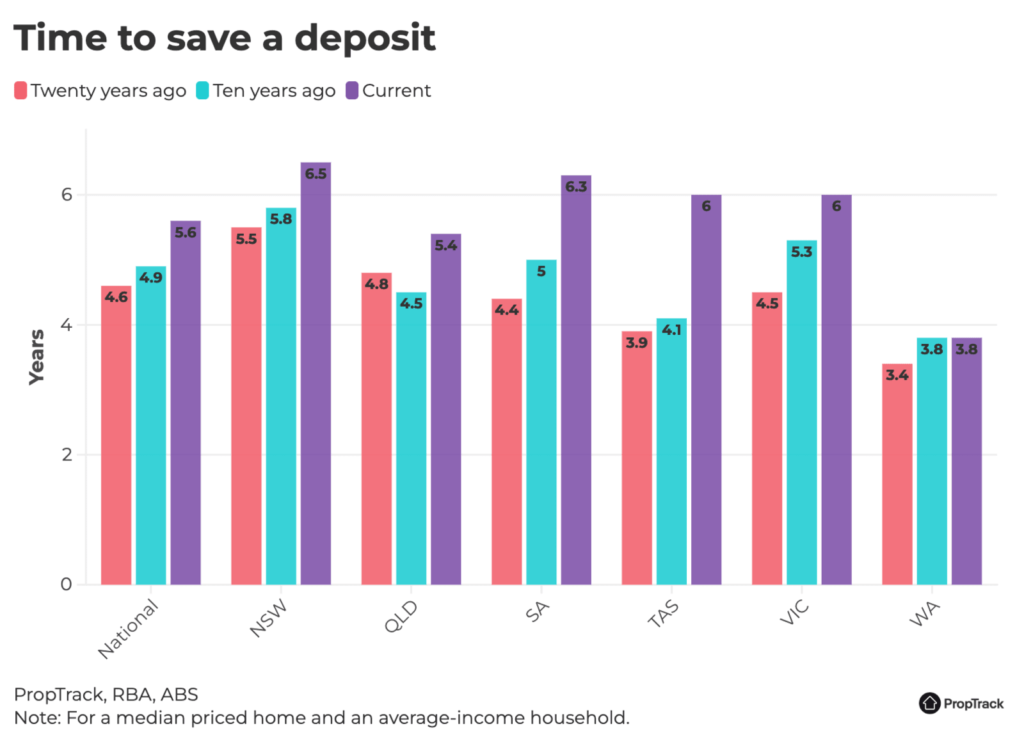

For many buyers, the biggest factor is the deposit. "Nationally, it takes around 5.6 years to save a deposit, a 14% rise compared to 10 years ago, but this figure varies across different states." This is why we focus on strategy rather than just saving.

Our Peak Wealth Insight

Giving up your daily coffee won't buy you a house in Sydney. We do not believe in stressing over unnecessary small daily costs that may impact your lifestyle more than your goals... That being said, we strongly reccomend having a budgeting strategy and action plan in place so you don't have to stress over the small things. Instead, we focus on your biggest fixed costs. Getting your housing and your mortgage interest right and adjusting your lifestyle where needed depending on your preferences and opportunities.

The Wildcard: The 2026-27 Federal Budget

Note: These are the proposed changes from the 2026-27 Federal Budget that was announced on May 12, 2026. This could change some of the rules for property investors quickly. To learn more about the Federal Budget changes, you can explore our complete Federal Budget breakdown here.

The government is narrowing the scope of negative gearing to encourage new housing supply.

- New Builds Only: From 1 July 2027, negative gearing will be restricted to "new build" residential properties.

- Established Properties: If you already own an established rental property (purchased before 7:30 pm on 12 May 2026), your current negative gearing arrangements are protected until the property is sold.

- Limited Deductions: For established properties purchased after last night's announcement, rental losses will only be deductible against other residential property income or future capital gains—not against your salary.

Our Peak Wealth Insight

We strongly advise our clients not to make rushed choices based on assumed changes. Do not panic-sell or rush into a purchase. Instead, let us model your numbers right now. We can model outcomes and discuss how this will impact you.

The Pros and Cons of Buying a Home

Owning a home offers many emotional benefits, but you must also look at the financial reality. Research shows that for most people, buying a home is a far better path to long-term wealth than renting (Source: Actuaries Institute).

The Pros of Buying:

- Full Control: You do not have to deal with landlords or rent hikes. You are in charge of your own home.

- Automatic Wealth Building: Every time you pay your mortgage, you pay off a little bit of your debt. This builds your wealth over time.

- Long-Term Growth: Australian property has a strong history of increasing in value over many years.

- A Place for Your Family: Owning a home gives you a deep sense of belonging. It is a stable space where your family can grow and make memories for years to come. That can be priceless for many families.

The Cons of Buying:

- Upfront Capital: You need a large deposit, plus money for stamp duty and legal fees.

- Ongoing Costs: Your mortgage is only the first cost. You should plan for thousands of dollars every year for council rates, strata fees, insurance, and keeping the home in good shape.

- Lower Liquidity: Selling a house takes time and costs money in agent fees.

Our Peak Wealth Insight

We see a common trap with the "Great Australian Dream." People often keep a strict budget while renting. But when they buy, they borrow the maximum amount possible. This can impact their cash flow and leave them with very little money for the rest of their life.

The Pros and Cons of Renting

Renting is a valid part of a wealth strategy in 2026. It works well if you are disciplined with your money. You can even use tools like the MoneySmart Rent vs Buy Calculator to see how the numbers look for your specific area.

The Pros of Renting:

- Monthly Cash Flow: In some major cities, a mortgage can cost significantly more than rent. Renting can free up your monthly money.

- Investment Opportunities: If you have a deposit saved, you can leverage that money in other areas, like the share market. These investments can grow very well as you assess your investment approach.

- No Maintenance Bills: The landlord is responsible for all major repairs.

- Mobility: You can easily move to a new area when your lease ends.

The Cons of Renting:

- No Direct Property Growth: You do not own the asset, so you do not get the profit when the house value goes up.

- Less Stability: The landlord might decide to sell the property or move back in.

- Savings Discipline: You only build wealth if you actually invest your spare money. If you spend it on lifestyle, you lose the advantage.

Our Peak Wealth Insight

Renting only builds wealth if you save your extra cash and then invest. We help our clients set up a budget and move their spare money into a separate "Future Fund." This keeps your wealth growing while you rent.

“Do not save what is left after spending; instead spend what is left after saving.”

— Warren Buffett

Government Help for Buying a Home

If saving a 20% deposit seems slow, the government has ways to help you get started in 2026. You can also learn more at firsthomebuyers.gov.au.

The Home Guarantee Scheme (HGS). This lets some buyers purchase a house with just a 5% deposit. This helps you avoid paying for mortgage insurance.

The First Home Super Saver (FHSS) Scheme lets you save money inside your superannuation. You pay less tax on this money. You can take out up to $50,000 to use for your deposit.

The Family Factor: Schools and Private Education

If you have children, the choice between buying and renting changes.

As most parents already know, getting into a top public school means you have to live within a strict local zone. Buying a home close to these schools often comes with a massive price tag.

On the other hand, private school fees are also a major financial commitment. It can cost tens of thousands and, in many instances, over $30,000 a year for each child.

This can create a cash flow challenge. If you put all your money into a huge home loan, you might find it hard to pay for the education you want for your children.

Our Peak Wealth Insight

We regularly map out school costs with our clients. For many families, the best choice is actually to rent in the strict school zone they need. This gets the kids into the right school and frees up cash flow without the pressure of a massive home loan.

Exploring "Rentvesting" in 2026

If you want to own property but cannot afford to buy where you want to live, "Rentvesting" is an option.

Rentvesting simply means you rent a home in a suburb that fits your lifestyle, like close to work or good schools. At the same time, you buy an investment property in a more affordable area.

This strategy is very attractive because it gives you the best of both worlds. You do not have to give up your ideal lifestyle just to get onto the property ladder. Your tenants help pay the mortgage on your investment, and you still build wealth as the property goes up in value.

This is usually a more attractive strategy for rather than trying to find properties that are cheaper (cash flow wise) to own than renting.

The 2026 Checklist: Should You Buy or Rent?

Before you make your next move, ask yourself these two questions:

- The 5-to-10 Year Rule: Can you keep the property for at least 5 to 10 years? Buying and selling property is a major financial event. Stamp duty and fees can cost 7% to 10% of the home's value. If you sell too soon, it is hard to make a profit.

- The 8.5% Stress Test: Do not look at the lowest rate available today. Ask yourself: Can I still pay this loan if rates go up to 8.5%?

Our Peak Wealth Insight

Simple online tools often miss the big picture. We use advanced financial planning and modelling to show you what your future looks like. Often, our clients choose the path that gives them more freedom, like taking family holidays. The numbers guide you, but the life you want makes the final call.

Conclusion: Stop Guessing, Start Forecasting

There is no single rule for renting and buying in 2026. It is about knowing your costs and finding the path that reaches your goals.

Renting builds wealth when you invest your extra cash. Buying builds value when you manage your debt at a safe level. Do not leave your biggest money decision to generic advice.

Stop guessing and start forecasting. Book a discovery call with us, Andrew Debono and Kristian Zuza, at Peak Wealth Management. We will help you map out a strategy that fits the life you actually want to live.

Frequently Asked Questions

There is no single answer. Buying gives you long-term security, but you need the capital for a deposit and ongoing costs. Renting is flexible and lets you invest your extra cash into other things (like shares), but only if you are disciplined with your savings.

Currently, interest rates and house prices mean a mortgage can cost much more than renting the same house. Renting allows you to keep your capital liquid and put it into investments that may grow faster than property.

Besides the deposit, you must pay Stamp Duty. After you buy, you will pay every year for council rates, strata fees, and maintaining the asset.

It depends heavily on where you live. In major cities, it can often take many years for a mortgage to cost less than renting. In more affordable regions, it might only take a few years.

Rentvesting is when you rent a house in a suburb you want to live in while buying an investment property in a more affordable area. It lets you live where you like while still building a property asset.