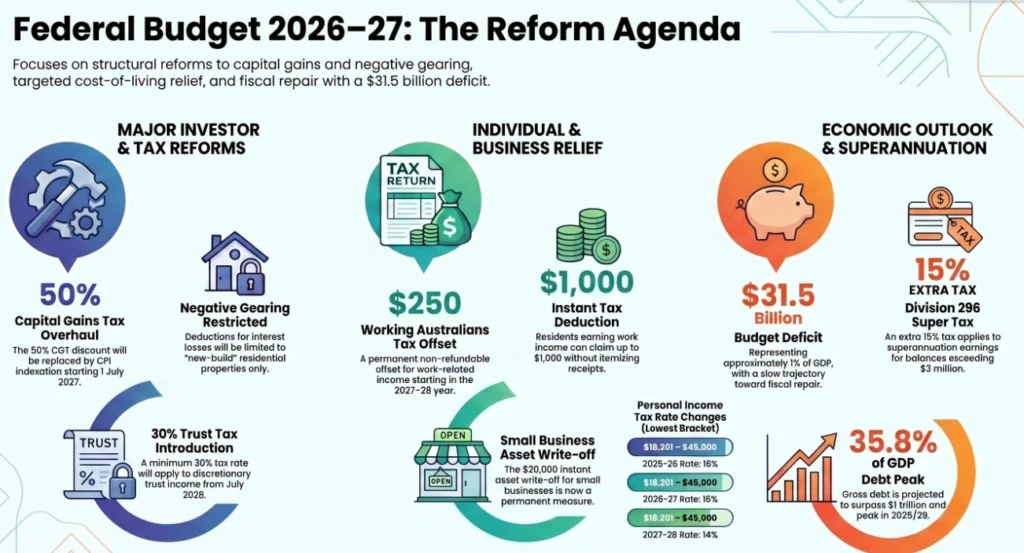

Last night, Treasurer Jim Chalmers handed down the 2026–27 Federal Budget. While the government has mentioned that they have focused on cost-of-living relief, there are several significant proposed reforms to Capital Gains Tax (CGT), negative gearing, and discretionary trusts that may impact your long-term investment strategy.

It is important to remember that these are currently proposals and not yet law. Here is a summary of the key highlights and how they might affect you.

We've tried to keep this summary short and to the point in an easy-to-digest format.

1. Major Capital Gains Tax (CGT) Reforms

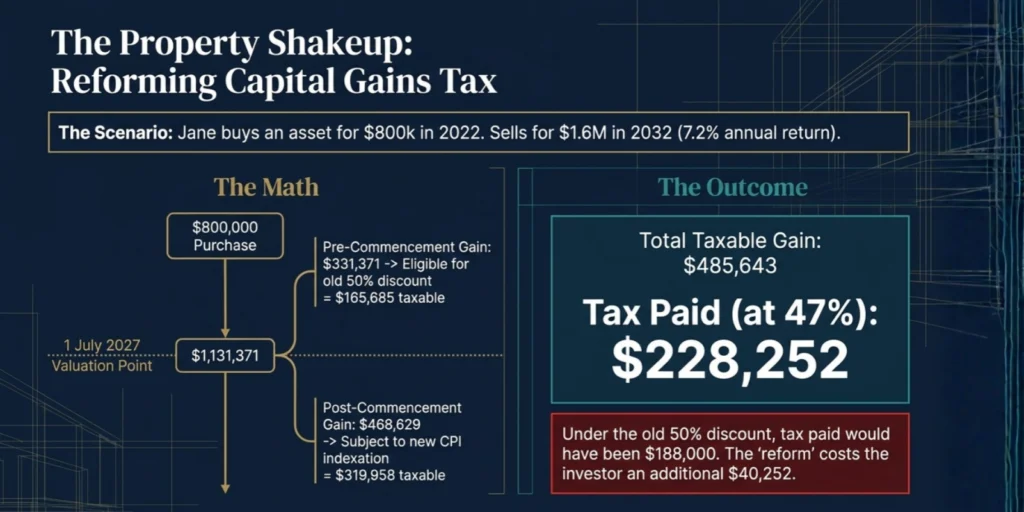

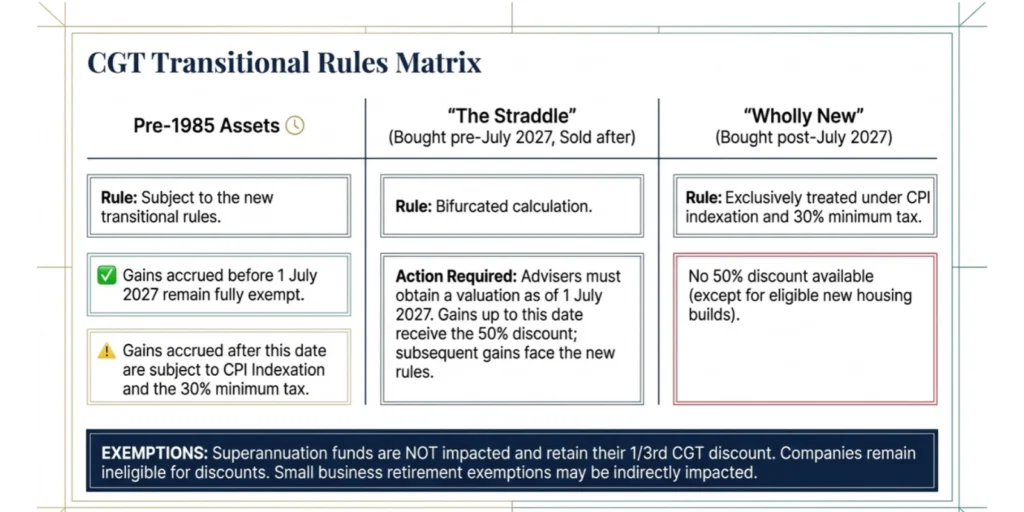

From 1 July 2027, the government intends to replace the current 50% CGT discount with a "cost base indexation" model, similar to the rules used before 1999.

- Indexation: Instead of a flat discount, your asset’s cost base will be adjusted for inflation (CPI) so you only pay tax on the "real"

- gain.

- 30% Minimum Tax: A new minimum tax rate of 30% will apply to realized capital gains. This aims to prevent taxpayers from waiting until retirement (when their income is lower) to sell

- assets and pay less tax.

- Transitional Rules: Assets you already own will be "grandfathered." Gains made up until 1 July 2027 will still be eligible for the 50% discount.

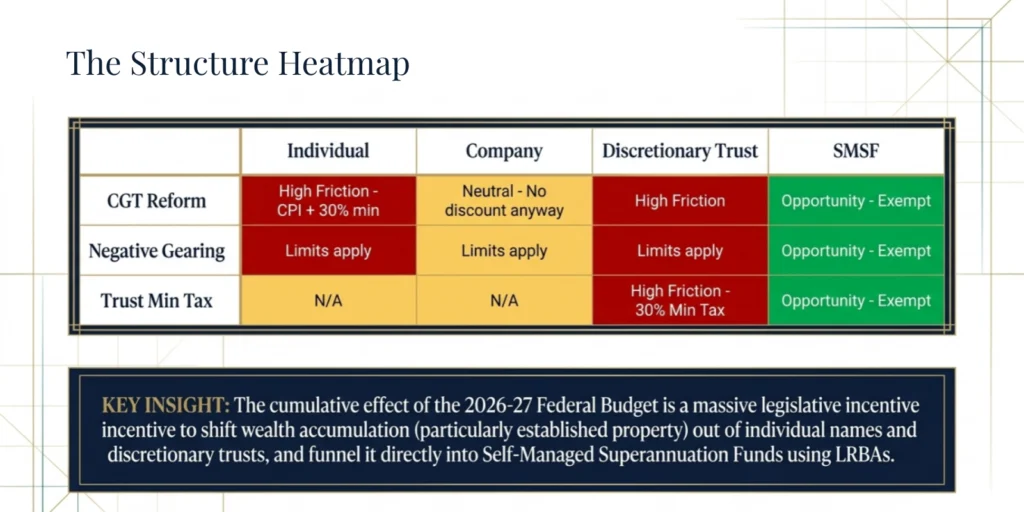

- Superannuation: Importantly, these changes do not apply to assets held within superannuation funds.

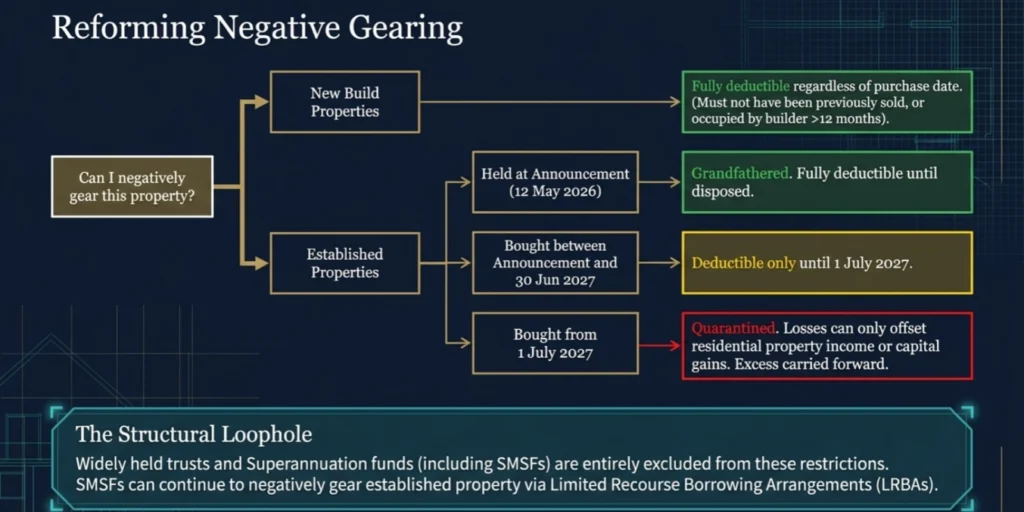

2. Changes to Negative Gearing

The government is narrowing the scope of negative gearing to encourage new housing supply.

- New Builds Only: From 1 July 2027, negative gearing will be restricted to "new build" residential properties.

- Established Properties: If you already own an established rental property (purchased before 7:30 pm on 12 May 2026), your current negative gearing arrangements are protected until the property is sold.

- Limited Deductions: For established properties purchased after last night's announcement, rental losses will only be deductible against other residential property income or future capital gains—not against your salary.

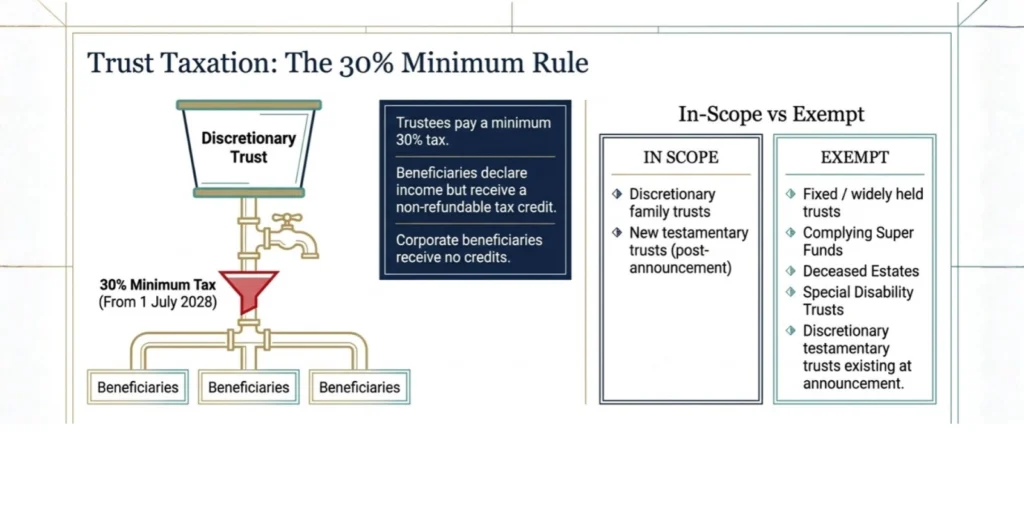

3. New Minimum Tax on Discretionary Trusts

From 1 July 2028, a minimum tax rate of 30% will be introduced on the taxable income of discretionary trusts.

- Trustees will pay this tax directly, and beneficiaries (excluding companies) will receive a non-refundable credit for the tax paid.

- Specific exemptions apply to deceased estates, charitable trusts, and special disability trusts.

4. Personal Tax Relief and Cost of Living

The Budget includes several measures to provide immediate relief to working Australians:

- $1,000 Instant Deduction: Starting 1 July 2026, you can claim up to $1,000 in work-related expenses without needing to keep receipts or itemise your claims.

- Working Australians Tax Offset (WATO): A new permanent tax offset of up to $250 per year will be available for income earned from work, effective 1 July 2027.

- Lower Tax Rates: The lowest marginal tax rate (for income between $18,201 and $45,000) will drop from 16% to 15% on 1 July 2026, and then to 14% on 1 July 2027.

5. Aged Care and Health

- Home Care: The government will fully fund "personal care" services (like dressing and showering) under the Support at Home program from 1 July 2026

- PHI Rebate: From 1 April 2027, the higher Private Health Insurance rebate for those over 65 will be removed to make the rebate consistent across all ages. This may increase out-of-pocket costs for some seniors.

Looking Ahead

Many of these changes—specifically regarding CGT and trusts—this may require you to review your current investment structures and timing for asset disposals.

We are also preparing for previously legislated changes starting this July, such as the indexation of superannuation contribution caps (the Concessional Cap will increase to $32,500) and the Division 296 tax for those with super balances over $3 million.

If you have any urgent questions, please don't hesitate to reach out on 02 9098 2341 or info@peakwm.com.au